Introduction

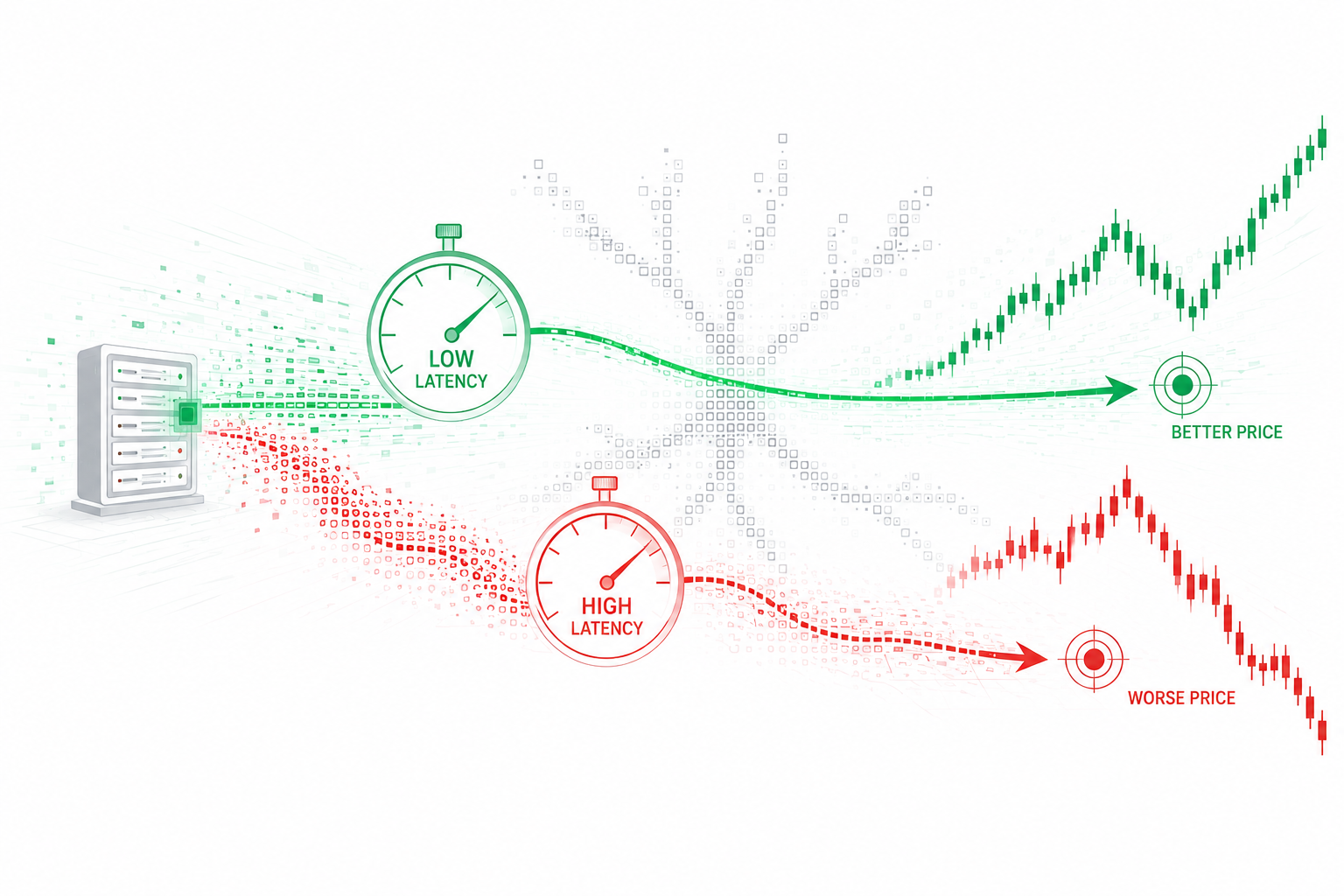

In traditional investing, latency is a minor convenience. In high-frequency trading (HFT), latency represents a probability distribution. Being a microsecond slower does not just mean a slightly worse fill. It often means a failed transaction or hitting adverse selection. Let's analyze how queue position shapes transaction economics.

Understanding HFT

Market makers sit on both sides of the order book, constantly quoting bid and ask prices. They profit from the spread but assume the risk of holding inventory. If the market moves, the market maker must cancel their stale quotes instantly. If they are slow, an arbitrageur will hit those stale quotes before they can be canceled. This is known as adverse selection.

Speed

To protect against adverse selection, risk limits must be evaluated inline for every single order. Since risk evaluation adds latency, engineers build pre-trade risk systems in hardware or highly optimized lock-free C++ functions. Here is a simple pre-trade risk check designed to execute under 50 nanoseconds on standard CPU architecture:

Benefits

Despite the risks, low latency HFT systems bring immense benefits to global financial markets. By executing millions of trades per second, they provide high liquidity and compress the bid-ask spread to fractions of a cent, lowering the cost of transaction execution for retail and institutional investors worldwide.

Challenges

However, extreme speed also amplifies systemic risk. If a trading algorithm has a logic error, it can submit thousands of faulty orders in milliseconds, triggering chain reactions and flash crashes across interconnected markets. Thus, strict pre-trade risk checks and automated circuit breakers are critical.

Future

The horizon of low latency is shifting toward hardware logic. High-frequency firms are compiling strategy rules directly into FPGA bitstreams using High-Level Synthesis (HLS) or SystemVerilog, bypassing CPUs entirely. In the near future, sub-nanosecond matching and quantum-inspired execution paths will redefine trading boundaries.

Conclusion

Latency is the currency of the financial execution layer. Achieving a low-latency edge requires a relentless focus on minimizing instruction counts, lock-free concurrency, and system-level validation to balance execution speed with risk safety.

Read More: To further understand the impact of low latency in HFT, check out my research project repository on GitHub: https://github.com/shaikhmubin02/hft-latency-research-project.git.